Regulatory Passporting and the Future of Cross-Border Fintech in Africa

Africa’s fintech giants are already regional, but regulation isn’t

When Nigerian fintech companies expand across Africa, the technology often travels easily. Payments APIs integrate quickly, merchants understand the products, customers adopt digital wallets and online checkout tools without much friction. Regulation, however, does not travel as easily.

A fintech that is licensed in Nigeria must often repeat the entire licensing process when entering another African market, navigating new capital requirements, compliance rules, reporting standards, and supervisory expectations. The result is a fragmented regulatory landscape that many fintech founders say slows expansion across the continent.

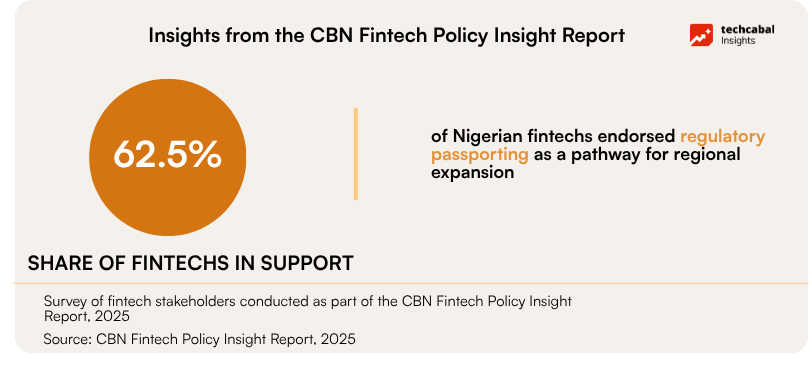

This challenge sits at the centre of the Central Bank of Nigeria’s Fintech Policy Insight Report, which explores the potential role of regulatory passporting in reducing duplication across jurisdictions.

According to the CBN survey, 62.5% of fintech stakeholders already operate in or plan to expand into other African markets, and the same share supports the development of a regulatory passporting framework.

The message from the ecosystem is clear: African fintech companies want to scale regionally. The question is whether the regulatory architecture of the continent is ready.

Infrastructure matters as much as regulation

Nigeria hosts one of Africa’s largest fintech ecosystems. Startups such as Flutterwave, Paystack, and Fincra now power payment infrastructure, merchant acquiring tools, cross-border settlement networks, and financial APIs used by businesses across multiple African markets. Yet each new market often introduces a different regulatory environment.

Fintech operators expanding regionally must secure local licences, meet jurisdiction-specific capital requirements, and build relationships with local banking partners and regulators. These processes can take months and sometimes years.

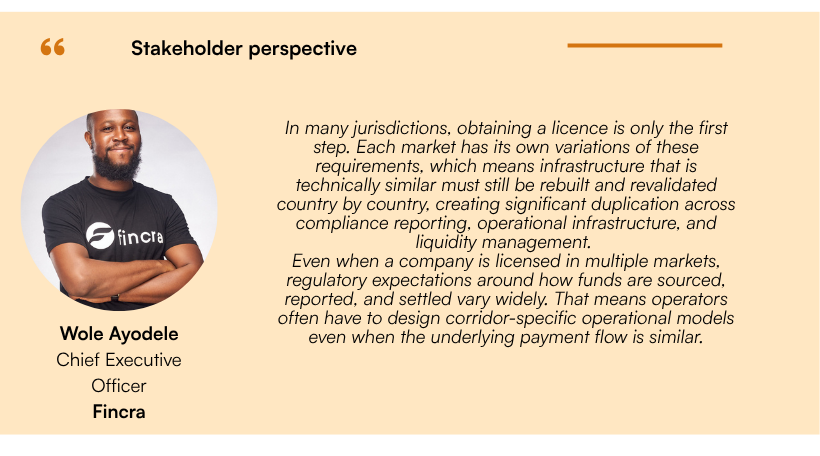

Passporting, Fincra argues, would also fundamentally reshape partnership models: by shifting relationships away from local intermediaries engaged purely for regulatory access toward partners focused on payment system connectivity, liquidity management, and settlement efficiency. But reducing licensing duplication, while necessary, may not be sufficient. Even operators who have cleared the regulatory hurdle find that the practical mechanics of cross-border payments introduce a separate layer of complexity.

Expansion ambitions meet regulatory fragmentation

Even when regulatory approval is secured, fintech companies must still navigate the practical mechanics of cross-border payments. These include foreign exchange constraints, liquidity management, settlement timing, and interoperability between payment systems. Nigeria’s domestic payments system offers an example of what coordinated infrastructure can achieve. The country’s instant payments network processed nearly 11 billion transactions in 2024, according to the Nigeria Inter-Bank Settlement System (NIBSS).

Nigeria’s scale is significant in global terms and has shown how large domestic payment rails can become foundational infrastructure for digital financial ecosystems.

Yet, scaling such systems across borders introduces new coordination challenges: from fraud monitoring and dispute resolution to identity verification and settlement oversight.

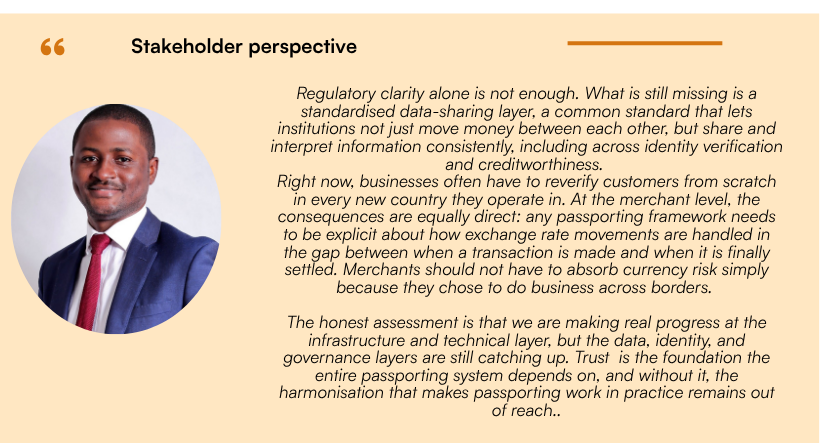

Transaction volume alone, however, does not define interoperability. In Paystack’s assessment, the gap between infrastructure progress and commercial reliability is where the most consequential work remains, particularly around data sharing, identity verification, and what merchants actually experience at the point of settlement.

Passporting may start with bilateral corridors

While passporting is often discussed as a continent-wide framework, the CBN report suggests that implementation may begin with smaller regulatory pilots.

Survey participants proposed exploring bilateral cooperation between Nigeria and several peer regulators, including those in Ghana, Kenya, South Africa, Uganda, and Senegal. Such pilots could test mutual recognition of licences while regulators coordinate supervisory standards and consumer protection frameworks. They could also allow countries to experiment with payments system interoperability, particularly between markets with strong digital financial ecosystems.

One example mentioned in the report is the possibility of testing interoperability between

Nigeria’s and Ghana’s payments systems to support real-time cross-border settlement. These experiments could complement continental infrastructure initiatives such as the Pan-African Payment and Settlement System (PAPSS), which aims to enable instant cross-border payments in local currencies across participating African markets.

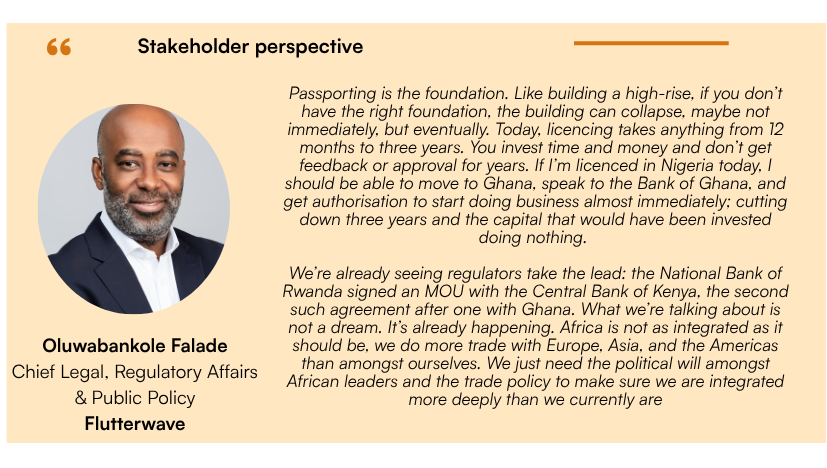

For operators who have navigated Africa’s licensing landscape firsthand, passporting is less a destination than a foundation. Flutterwave, which has expanded across multiple African markets without a passporting framework in place, sees the bilateral corridor model as the right sequencing.

How passporting works in other financial markets

The idea of regulatory passporting is not unique to Africa. In the European Union, financial institutions licensed in one member state can operate across the bloc under passporting frameworks embedded in regulations such as MiFID II. This system allows banks, investment firms, and fintech companies to provide services across 27 EU countries without having to secure a licence in every country.

The European Union’s Undertakings for Collective Investment in Transferable Securities (UCITS) framework, for example, allows investment funds authorized in one member state to be marketed across the entire bloc, while Singapore’s Monetary Authority has pursued cross-border regulatory cooperation agreements to support fintech innovation.

These precedents matter for Africa, but they do not translate directly. The EU’s passporting architecture was built on decades of regulatory convergence across economies with comparable institutional maturity. African regulators are now exploring whether similar coordination models can work across a continent with far more diverse regulatory environments, deeper infrastructure gaps, and a much shorter history of cross-border supervisory cooperation. The operators and investors who have engaged most closely with this question are clear that the concept is sound, but that the conditions which made it work elsewhere will need to be deliberately constructed here, not assumed.

Why regulatory alignment matters for Fintech capital

Beyond operators and regulators, passporting also matters for capital. African fintech startups attracted $1.38 billion in venture investment in 2025 alone, yet investors continue to weigh regulatory complexity when assessing cross-border expansion strategies.

Growth investors often evaluate markets not only on demand and revenue potential, but also on regulatory predictability and the cost of expansion. However, regulatory alignment alone does not determine fintech success.Market depth, customer adoption, and strong product execution remain decisive factors.

In that sense, passporting may reduce friction in scaling across markets, but it does not replace the fundamentals that ultimately drive company performance.

As Lexi Novitske, partner at Norrsken22, noted in response to the CBN report, the practical implementation of new regulatory frameworks will matter as much as the concept of passporting itself

For investors, the decisive question is therefore not simply whether passporting would work, but whether it reduces uncertainty or compounds it.

Passporting requires regulatory coordination

Implementing passporting frameworks requires more than just regulatory agreement. Participating jurisdictions must align supervisory practices, legal frameworks, consumer protection standards, and technical infrastructure. This coordination becomes more complex as more countries participate.

The CBN report acknowledges that such frameworks cannot be implemented unilaterally. Instead, they require collaboration between regulators, payment system operators, infrastructure providers, and fintech companies themselves.

For many observers, the conversation around passporting reflects a broader shift in Africa’s fintech ecosystem. A decade ago, the sector’s primary challenge was building digital payment products that people would use. Today, the challenge is often scaling those products across borders.

The next phase of Africa’s Fintech expansion

Africa’s fintech ecosystem has grown rapidly over the past decade, supported by increasing smartphone adoption, expanding internet access, and rising demand for digital financial services. The next phase of growth may depend less on technological innovation and more on institutional coordination.

Regulatory passporting represents one potential step toward that coordination.

Whether it succeeds will depend on the willingness of regulators to align frameworks, the readiness of infrastructure providers to support interoperability, and the ability of fintech companies to operate responsibly across multiple jurisdictions.

The CBN Fintech Policy Insight Report does not present passporting as an immediate solution. Instead, it frames it as part of a longer-term conversation about how African financial markets can become more integrated. For fintech founders, investors, and regulators alike, that conversation may shape the next chapter of Africa’s digital financial ecosystem.

Ayrıca Şunları da Beğenebilirsiniz

Trump biographer predicts next 3 Cabinet members on the chopping block

Kalshi hires ex-Democratic strategist amid legal troubles